The conflict in Iran rewrites the global broiler map. China is now the world’s fourth-largest poultry exporter: Rabobank depicts a sector in accelerated reconfiguration

The just-published RaboResearch quarterly report for Q2 2026 identifies the Middle East conflict as the greatest global structural challenge for poultry meat in 2026, with direct impacts on trade, feed, food security and producer margins

A strong market stumbling over geopolitics

The global poultry industry enters Q2 2026 with solid fundamentals: global chicken consumption will grow between 2.5% and 3% this year, exceeding the historical average of 2.4%. Asia-Pacific and South Asia are leading the expansion, and Europe is also recording robust consumption despite operational difficulties caused by avian influenza.

But the RaboResearch report raises an unambiguous alert: the Middle East conflict — with the Strait of Hormuz as its epicentre — is introducing a level of volatility the sector has not faced in decades. The impact is articulated along four vectors: global economic slowdown, inflationary pressure on consumers, rising fertiliser and grain prices, and disruption of trade flows.

“Chicken will remain the winning protein in 2026, but geopolitics has ceased to be background noise and has become a determining variable for margins and volumes.”

This is not new at NeXusAvicultura. In previous analyses of the broiler sector we had already anticipated that geopolitics would be the factor most affecting poultry in 2025 and 2026, and that countries would prioritise food sovereignty over producing chicken for export. The new report confirms and amplifies that thesis.

The Strait of Hormuz: the artery nobody wanted to notice

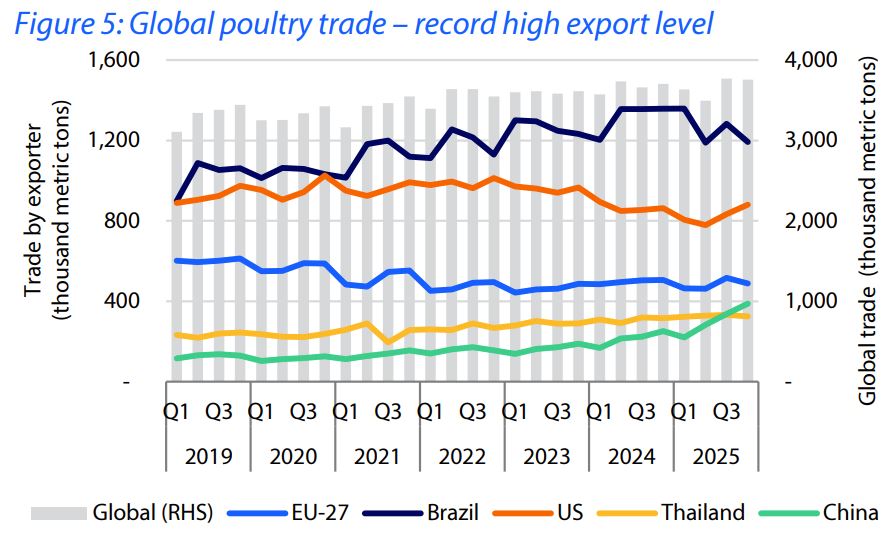

The Middle East accounts for 15% of global poultry trade and is the destination for 35% of the value of Brazilian chicken exports. If the Strait of Hormuz remains blocked or under prolonged tension, the consequences are symmetrical in both directions: Gulf countries — which depend on imports for more than 50% of their chicken supply, and to an even greater degree for genetic material and feed raw materials — see their food security threatened, while Brazil, the EU, Ukraine and Russia lose their principal export market.

Rabobank notes that Saudi Arabia can partially redirect its supply via western routes, but the situation is far more fragile for Qatar, Kuwait and the UAE. Brazilian shipments already in transit have had to be rerouted or are awaiting authorisation to unload, generating internal oversupply in Brazil and downward price pressure at origin.

Brazil: record exports with feet in the mud

The paradox of Brazilian poultry aptly illustrates the complexity of the moment. February 2026 was the best month in history for chicken exports: 493,000 tonnes (+8% year-on-year) valued at USD 945 million (+9%). The January–February cumulative total exceeded 940,000 tonnes and USD 1.8 billion. Nevertheless, the outlook for Q2 2026 remains uncertain.

The Gulf region accounted for 9% of Brazilian exports in the first two months of the year and also acts as a critical logistics route to Asia. The conflict is not merely a demand problem: it raises freight costs, distorts delivery schedules and forces destination routes to be reconfigured on the fly. South Africa (+31% year-on-year in purchases from Brazil) and the UAE remain stable anchors, but they do not offset the Chinese pullback (-12% year-on-year) or the uncertainty across the Middle East.

“Chicken will remain the winning protein in 2026, but geopolitics has ceased to be background noise and has become a determining variable for margins and volumes.”

China: from net importer to global exporter

The report devotes particular attention to China’s structural transformation. Chinese poultry production grew 6.7% in 2025, reaching a record 28.3 million metric tonnes, and exports surged 50% year-on-year, driven by breast meat. China has overtaken Thailand in the global ranking and has become the world’s fourth-largest chicken exporter.

The price differential is the market weapon: while processed Thai chicken is priced at around USD 4,500/tonne, the Chinese product is offered at approximately USD 3,500/tonne. This gap is eroding Thailand’s global market share and putting pressure on producers in every country where Chinese chicken lands at aggressive prices — including certain European markets via indirect imports.

However, the closure of the Strait of Hormuz has temporarily halted Chinese exports to the Middle East (12% of its total exports), generating internal inventory build-up and short-term downward pressure on the Chinese domestic market.

“China has become the world’s fourth-largest chicken exporter, with processed product prices 22% below Thai competition. The disruption is already structural.”

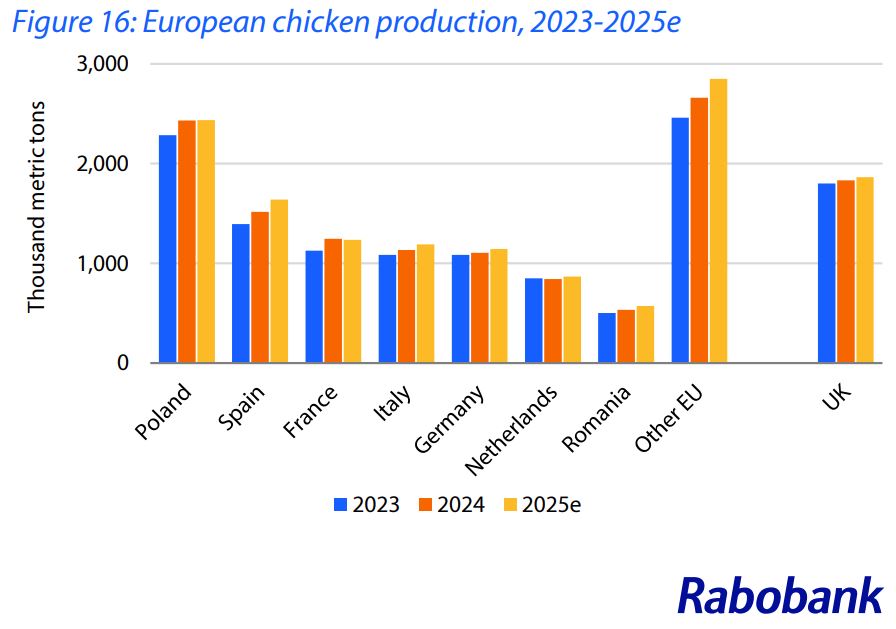

Europe: strong, but not insulated

Europe is one of the best-performing markets in this report. Consumption grew by almost 3% in 2025, live chicken prices in the EU remain above 2024 levels (USD 1.62/kg in Q1 2026 forecasts), and the competitive position of European chicken against beef — at historically high prices — continues to be a structural advantage.

The weak points are well known: highly pathogenic avian influenza continues to hit north-western Europe and Poland, the availability of hatching eggs and day-old chicks is at historic lows (limiting growth), and the Middle East conflict is exerting indirect pressure on European consumer purchasing power through energy prices. Spain, Italy, Greece, Romania and Hungary are the production growth hubs on the continent.

“Europe is holding up well, but it is not immune: the Middle East crisis is squeezing consumers’ wallets through energy.”

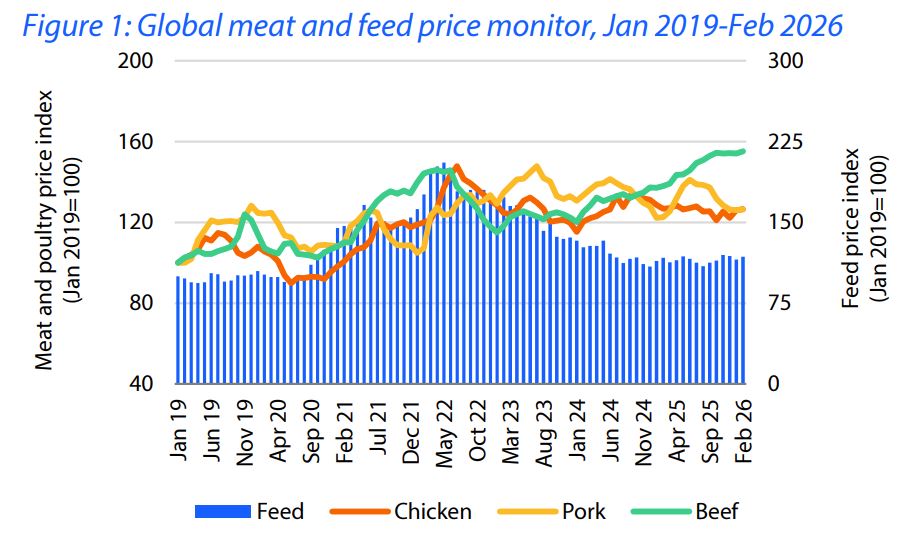

Feed: relative stability with upside risk

Grain and oilseed prices enter Q2 2026 with mixed but manageable dynamics. Maize is holding within a contained range thanks to ample global supply and a record soybean harvest in Brazil. However, the Middle East conflict is introducing upward pressure through fertiliser markets: Gulf nations are key suppliers of nitrogenous and ammoniacal fertilisers, and their prices have already begun to rise. If this trend consolidates, the impact will feed through to agricultural production costs in the 2026–2027 season.

Rabobank projects maize at around USD 475–488/bushel in Q3–Q4 2026, and soybeans potentially settling between USD 295–305/tonne. These are manageable scenarios, but subject to revision should the conflict be prolonged.

Avian influenza: endemic and migrating towards the southern hemisphere

nnnnHPAI remains the sector’s greatest operational biological risk. In the first months of 2026, FAO has recorded active outbreaks in 39 countries. In the U.S., more than 4.8 million birds were affected at the start of the year, with mass culls in Colorado (1.3 million) and Pennsylvania (1.5 million). Europe culled more than 2.8 million birds in January alone due to outbreaks in the northwest of the continent and Poland.

nnnnThe pattern that most concerns epidemiologists is the progressive endemisation of the virus: HPAI is increasingly behaving as a permanent risk in both wildlife and production systems. With the arrival of spring in the northern hemisphere, the risk migrates southward—Brazil, South Africa, Argentina—where the colder months from May to September will increase transmission pressure.

nnnnnnnn

Mercosur-EU: the agreement that arrives at the worst possible time

nnnnRabobank confirms that the Mercosur-EU trade agreement is expected to enter into force in 2026, with possible provisional application from 1 May. This will increase the volumes of chicken exported from Brazil, Argentina and Uruguay to the EU, adding competitive pressure on European producers already strained by HPAI costs and breeder availability.

nnnnAt NeXusAvicultura we have closely followed the implications of this agreement. You can read further analysis in our dedicated article: Mercosur: where do we stand now and what comes next?

nnnnnnnn

The best- and worst-performing markets

nnnnBest positioned: Europe (especially south and east), Thailand (exports), India, Indonesia, the Philippines and South Africa.

nnnnUnder greatest pressure: U.S. (oversupply, chicken prices 16% below 2025), Brazil (export distortion due to the conflict), Mexico (domestic oversupply + Brazilian import competition) and China (excess domestic production depressing local prices).

nnn

nnnn

Summary of the main figures in the global chicken sector for the second quarter of 2026

nnnn| Indicator | Key figure |

|---|---|

| Global consumption growth 2026 | 2.5%–3% (vs. historical average 2.4%) |

| Global trade growth | +1.2% (limited, more price-driven) |

| Brazilian exports January–February | 940,000 t / 1,800 M USD (+6%/+9% y-o-y) |

| Chinese exports 2025 | Has gone from being a net importer to becoming the 4th largest exporter in the world |

| Active HPAI outbreaks (FAO) | 39 countries, endemic pattern |

| EU live chicken prices Q1 2026 estimate | 1.62 USD/kg |

| Brazil live chicken prices Q1 2026 estimate | 0.97 USD/kg (-12.3% vs Q4 2025) |

| Maize (Q4 2026 forecast) | ~488 USD/bushel |

| Main geopolitical risk | Strait of Hormuz / Iran conflict |

| Mercosur-EU agreement | Provisional application expected from 1 May 2026 |

nnn

Follow-up at NeXusAvicultura

nnnnThis report is part of the series of analyses that NeXusAvicultura publishes on the poultry meat sector. You can browse all our previous articles on the global poultry meat sector at https://nexusavicultura.com/tag/sector-carne/

nnnnWant to stay one step ahead in poultry farming?

Subscribe free to our eNewsletter and receive a weekly selection

of the best information to anticipate trends, stay up to date and grow as a poultry industry professional.

NeXusAvicultura: Vision, Criteria, Quality and Context.

nnnnnnnn

Source:

-. Global poultry quarterly Q2 2026: Solid global chicken demand, rising geopolitical risks and volatility. 31 March 2026. Rabobank Report.

To find out more:

-. Poultry farming in Europe

-. Global poultry meat consumption

-. 2025 map of the poultry meat sector: key trends

nnnnnnnnn