2026 Outlook for Global Broiler Production: A bullish year in which countries will prioritise “Food Sovereignty” over producing chicken for export

Editorial Team, NeXusAvicultura.com

The global poultry market is preparing for another year of robust expansion. However, as industry professionals, we cannot allow ourselves to be carried away solely by the optimism of growth figures; operational and geopolitical volatility will be the norm. According to the latest Rabobank report for the first quarter of 2026, global growth of 2.5% is projected, continuing the positive trend of the past three years during which worldwide chicken meat consumption has grown by around 3%.

Below, we break down the critical factors that will define success in our industry over the next twelve months.

Growth drivers and new consumption trends

The fundamental outlook for poultry meat remains solid. Growth in consumption is not only supported by traditional drivers — such as the competitive price relative to beef and egg shortages — but also by improved economic conditions in key markets such as Asia, Africa, and Latin America.

“Europe will see production growth, shifting further towards the south and east of the continent.”

One fascinating finding revealed by the report is the influence of modern health trends. The rapid rise in the use of GLP-1 medications for weight reduction could boost chicken consumption, as this protein forms an essential part of the diets recommended under these treatments. Nevertheless, production growth (2.5%) will outpace global trade growth (1.5%–2%). This reflects a structural shift towards food security policies, where governments prioritise “local for local” production over imports.

Production efficiency and preparedness for unexpected geopolitical volatility and an Avian Influenza that is here to stay.

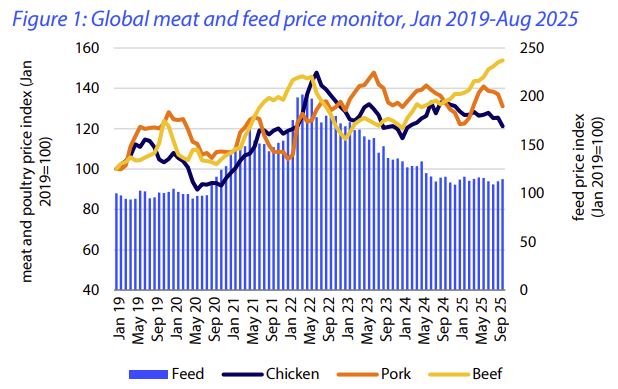

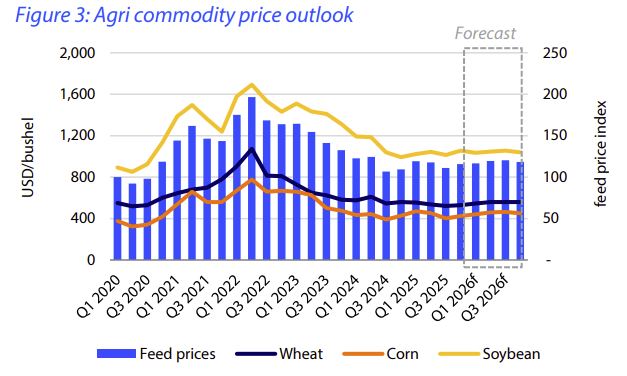

The message for producers in 2026 is clear: operational excellence must be the primary focus. Although the outlook for feed prices is relatively flat and positive, the situation can change rapidly due to climatic factors in the northern hemisphere.

“Global trade will grow (1.5%–2%) at a slower pace than total production, reflecting protectionist policies.”

The two major disruptors to watch are:

- Avian influenza: The current high-pressure situation in the northern hemisphere should serve as a wake-up call. The virus has the potential to significantly impact local production and trade if the avian influenza pandemic continues to spread through the winter.

- Geopolitics: Trade tensions and potential new agreements (such as the EU–Mercosur deal or US reciprocal tariffs) could redraw trade flows overnight.

Table 1: Situation summary by key region

We have summarised the situation in the main global markets for 2026 based on 2025 data:

| Region / Country | Price trend | Production outlook | Key factor to watch |

| United States | Stabilising after seasonal decline | Moderate (+1.5% to 2%) | Margin recovery and foodservice demand. |

| European Union | Strong but volatile | Recovery (+2% to 3%) | Avian influenza risk and supply discipline. |

| Brazil | Rising in live chicken | Strong export recovery | Climate (La Niña), logistics, and lifting of trade bans. |

| China | Under pressure due to oversupply | High, driven by prior capacity expansion | Imports will rebound after lifting of ban on Brazil. |

| Thailand | Strong (despite recent decline) | Growth (+2.5%) | Labour shortages and Chinese competition in processed products. |

| South Africa | High prices (+7%) | Tight supply | Chicken remains the most affordable protein compared to beef. |

Positive global outlook, but with regional differences

The big winner in global chicken trade in the third quarter of 2025 was China, which continued its strong growth as a key chicken exporter, particularly in processed products. China’s total chicken export volume grew by 50%, reaching 340,000 metric tonnes in Q3 2025, surpassing Thailand to become the world’s largest poultry exporter. Very low domestic chicken prices in China, compared with international prices, are helping the country gain market share in global trade. Other winners include Turkey (+44% growth), the EU (+2%), as well as Russia and Ukraine.

“In China, the rapid expansion of rearing capacity has generated an oversupply that is pushing prices below cost.”

Americas: recovery and adjustments

In Brazil, the export giant, shipments reached their second highest volume on record in October 2025. Having been declared free of avian influenza, the country is well positioned to gain market share, although it must monitor the climatic effects of La Niña in the south, which could complicate logistics and input supply.

In the United States, chicken prices are expected to rebound in 2026 thanks to a moderation in supply growth and stronger demand in the foodservice sector. Margins should improve on the back of grain availability.

Mexico, for its part, faces the need to rebalance its market. Prices fell to historic lows in Q3 2025 due to an internal oversupply, exacerbated by record imports from Brazil (+58%).

“Geopolitics and food security are leading governments to prioritise local production over international trade.”

Asia: keep an eye on China’s emerging processed products industry

China presents a complex scenario. Production has grown rapidly (+7.2% in the first three quarters of 2025), which has pushed prices downward, placing them below the break-even point for many independent producers. However, imports are expected to recover following the lifting of the ban on Brazilian chicken. China is also becoming an aggressive exporter, recently surpassing Thailand as the world’s fourth largest exporter thanks to its competitive prices in processed products.

Japan maintains solid demand driven by consumer preference for convenience and value, although yen depreciation remains a factor to consider with regard to imports.

“The surge in GLP-1 weight-loss medications could unexpectedly boost chicken consumption as a recommended dietary protein.”

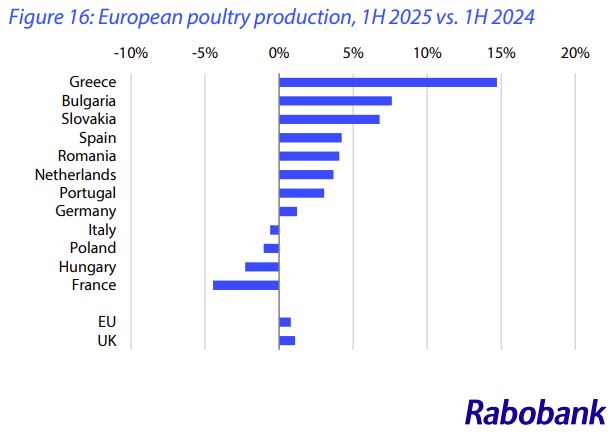

Europe: strength with caveats

The European poultry sector is enjoying strong market conditions, with potential annual growth of 2% to 3%. However, the recent wave of avian influenza outbreaks in north-west Europe and Spain poses immediate risks to supply, particularly if it affects breeder flocks, which would put strain on the global genetics supply chain.

“The market will grow by 2.5%, driven by improved economic conditions in emerging markets and the competitive price relative to beef.”

Table 2: Cut price dynamics (Recent trends)

Below, we present how prices for specific cuts have performed in key wholesale markets, reflecting the volatility mentioned above:

| Product | Market | Recent trend | Observation |

| Whole chicken | Brazil (Wholesale) | Decline (-7.1%) | Recovery expected towards year-end. |

| Whole chicken | EU (Wholesale) | Rise (+4.0%) | Strong market due to tight supply. |

| Breast | EU (Poland) | Slight decline (-3.0%) | Correction after previous record prices. |

| Leg quarters | USA (Northeast) | Stable (+1.7%) | Steady export demand. |

| Feet | China (Import) | Decline (-5.8%) | Pressure from ample local supply. |

At NeXusAvicultura.com, we will continue to report promptly on how these trends impact your day-to-day business. 2026 will be a year of opportunities for those who manage information proactively.

Source:

-. Global poultry quarterly Q1 2026: Another bullish year for poultry, but with more market volatility. 6th january 2026. Rabobank Report.

Further reading:

-. Poultry farming in Europe

-. Global poultry meat consumption

-. 2025 map of broiler production: key trends

Want to stay one step ahead in poultry?

Subscribe free to our eNewsletter and receive a weekly selection

of the best information to anticipate trends, stay up to date, and grow as a poultry industry professional.

NeXusAvicultura: Vision, Insight, Quality and Context.